Willem Veldhuyzen

Willem Veldhuyzen No Comments

No Comments May 14, 2026

May 14, 2026Key Takeaways

- Verify the collection statute expiration date using IRS account transcripts before choosing any installment agreement or resolution path

- Request Currently Not Collectible status when hardship is documented, knowing IRS collection can resume when finances improve

- Pursue an Offer in Compromise knowing the pending period suspends the statute — even a rejected offer pushes the CSED later

- File any Substitute for Return years with an accurate original return to correct the assessed balance before the CSED closes

- PriorTax helps taxpayers file back taxes accurately and affordably, with transparent pricing and no hidden fees

Most people asking about old tax balances want one answer: when does the IRS lose the legal right to collect? Understanding the IRS 10-year statute of limitations starts with one critical distinction: this rule usually limits IRS collection of assessed tax, not filing deadlines, audits, or when the Internal Revenue Service can review a return.

This article explains when the clock starts, what pauses it, how penalties and interest fit in, and how to verify the real expiration date from your records instead of guessing from IRS notices.

What the 10-Year IRS Collection Rule Actually Means

The 10-year rule usually applies to unpaid taxes the IRS has already assessed.

Once that collection period expires, the Internal Revenue Service generally cannot keep using enforced collection tools to pursue that assessed balance, even if penalties and interest made the debt much larger over time.

That point matters because many taxpayers confuse collection deadlines with the due date of the return. The rule is not automatic forgiveness based on April filing deadlines, and it is not triggered simply because you owe for an old year.

IRS Publication 1 explains taxpayer rights during collection, and one of the most practical is the right to know where you stand in the process. If the government’s collection period has expired, the IRS should stop collection on that assessed amount, but suspension of the statute can push the deadline later than expected.

IRS notices often mention balances due without clearly teaching the timeline behind them.

A notice showing an old tax year does not prove the 10 years have run, because the legal clock usually follows assessment, not the tax year printed on the letter.

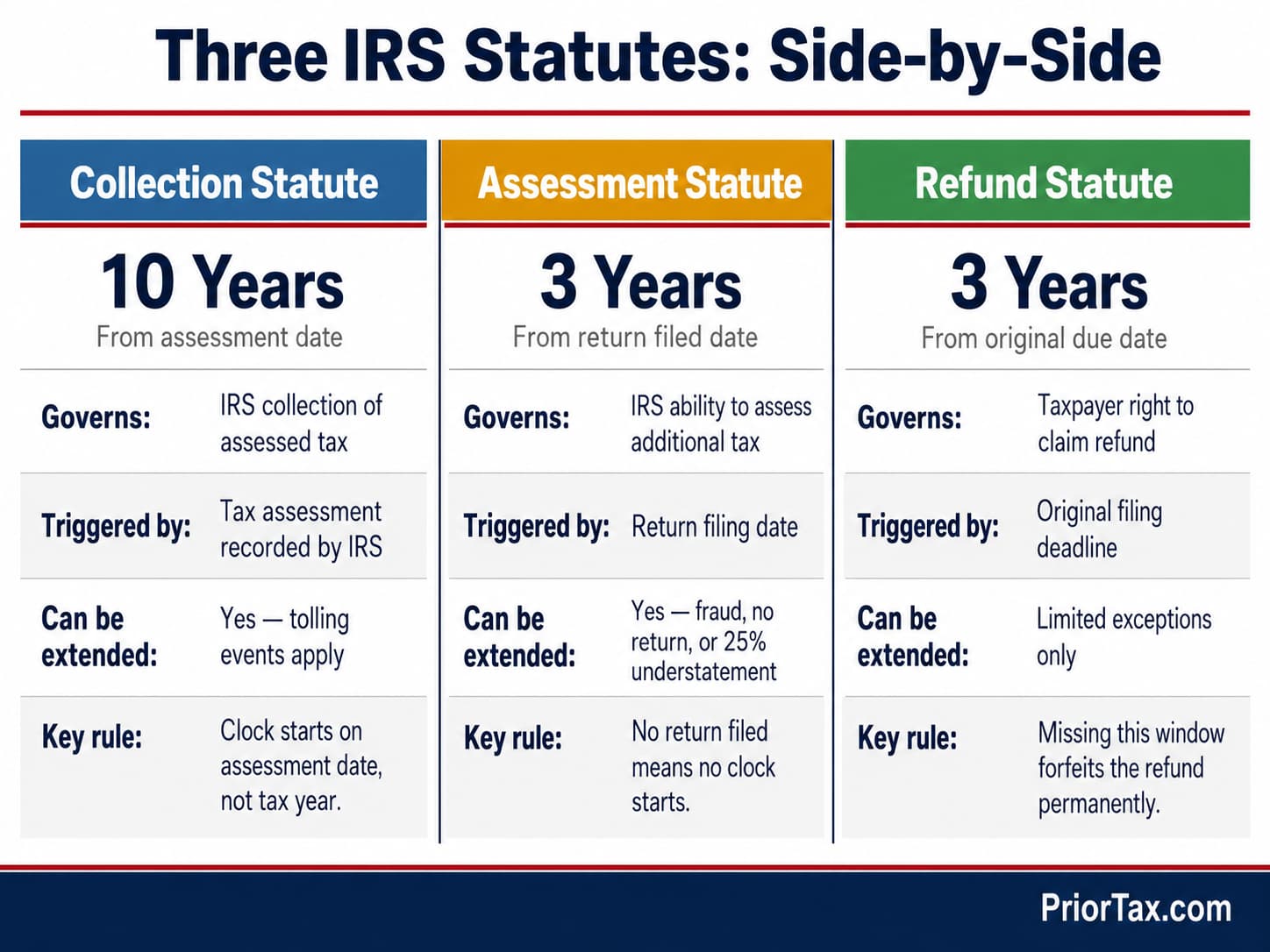

Collection vs Assessment vs Refund Statutes

The collection statute expiration date, or CSED, is usually 10 years from the assessment date.

The assessment statute is different and is commonly three years, though no return, fraud, or substantial understatement can extend or remove that limit.

The refund statute is also separate and is generally three years to claim money back. A payment plan may help manage collection, but it does not erase the difference between collection, assessment, and refund deadlines.

When the 10-Year Clock Starts: The Assessment Date

The clock usually starts on the assessment date, not the tax year and not the original filing deadline.

A tax assessment is the IRS’s formal recording of a liability on its books, and that bookkeeping event is what gives the government a collection window.

That detail changes real cases. Someone may owe for a 2016 return, file late in 2019, and see the collection period tied to a 2019 assessment rather than the 2017 due date.

Assessment often happens after the IRS processes a filed return showing a balance due. It can also happen after an audit adds tax, or after the IRS creates a liability through enforcement procedures.

Examples of Assessment Triggers

A filed return with tax due usually leads to assessment after processing. Audit changes create assessment when the examination is finalized and the added tax is entered.

An SFR, short for Substitute for Return, is another common trigger. When the IRS prepares an SFR using income data it has on file, the assessed amount is often higher because deductions and credits may be missing.

How to Find Your CSED (Collection Statute Expiration Date)

The date most taxpayers care about is the CSED, because it marks when the IRS’s normal collection authority ends for a specific assessment.

The Taxpayer Bill of Rights includes the Right to Finality, which means you are entitled to know how long the IRS has to collect and when that period ends.

The most reliable source is an IRS account transcript. You can access transcripts through your IRS online account when available, or request them by mail if online access fails.

Do not estimate from memory or from the tax year on a notice.

The Taxpayer Advocate Service regularly deals with cases where taxpayers relied on the wrong start date and misunderstood whether collection was still open.

Using an IRS Account Transcript

Look for assessment entries, transaction dates, and later events that may have suspended collection.

A transcript gives a paper trail, which is far stronger than trying to reconstruct dates from old letters.

Why the “10 Years” Is Often Longer in Practice

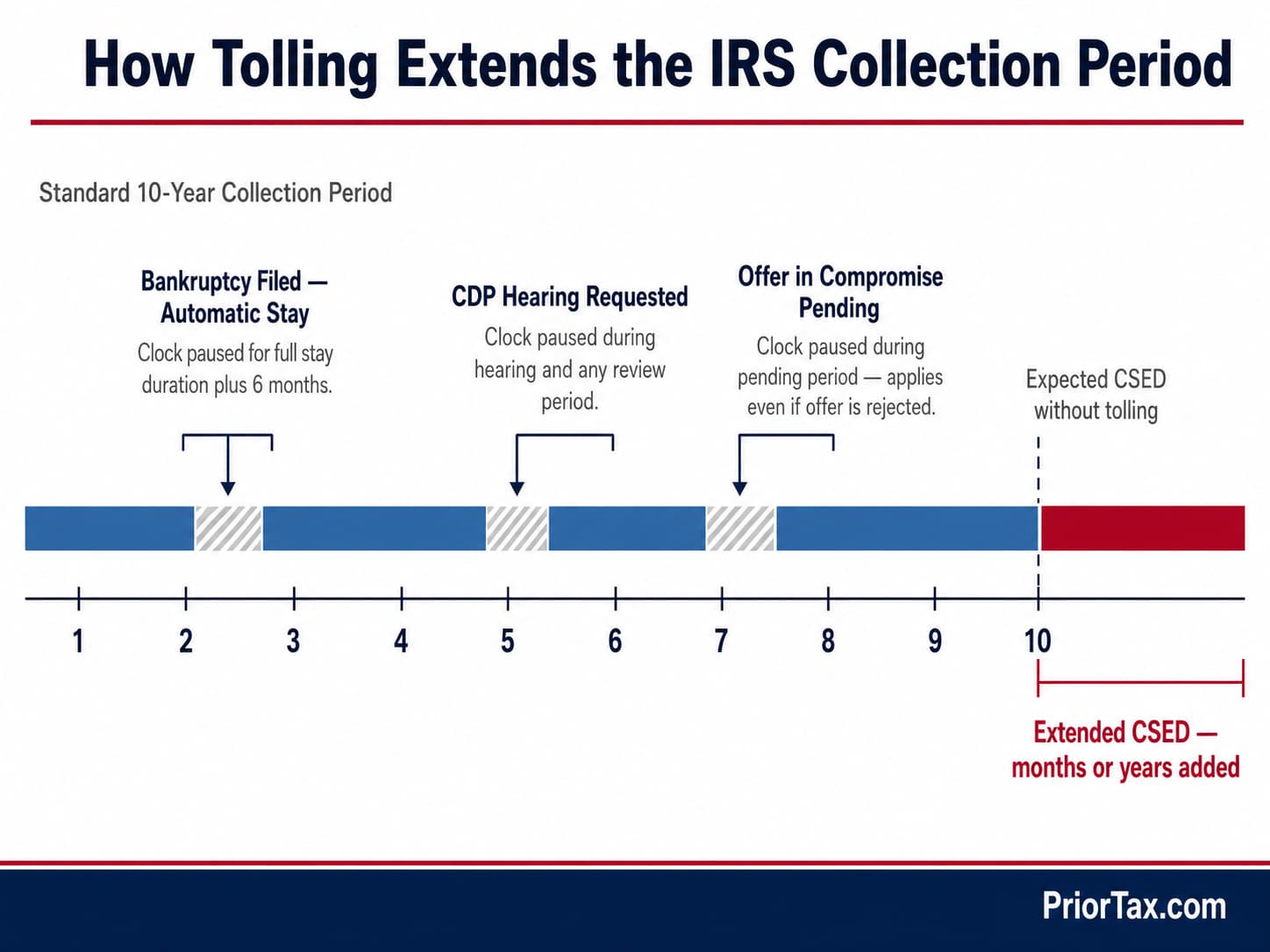

The phrase “10 years” sounds fixed, but the actual period can stretch. Tolling events pause the clock, and multiple assessments for one tax period can create more than one CSED.

What Pauses or Extends the 10-Year Collection Period

Tolling means the collection clock stops running for a legally defined period. That pause can add months or longer to the IRS collection window, which is why old balances often survive past the date taxpayers expect.

Bankruptcy is one of the biggest tolling events because the automatic stay blocks collection while the case is active. A collection due process hearing request can also suspend collection time while the appeal is pending.

An “Offer in Compromise” has similar effect. If the offer is pending, the IRS generally pauses collection, and extra time may be added after rejection or withdrawal.

Common Tolling Events to Know

Bankruptcy affects the CSED in two distinct ways.

The automatic stay pauses collection and extends the statute while the case is active.

Separately, Chapter 7 and Chapter 13 filers may be able to discharge qualifying income tax debts entirely if the taxes meet a set of eligibility tests, one of which requires that the return was due at least three years before the bankruptcy filing date. A discharged debt is eliminated, not deferred, so the 10-year collection window stops applying to that balance.

CDP hearings usually suspend the statute during the hearing and any related review period.

Offer in Compromise timing matters just as much as the result. A rejected offer still can push the collection deadline later because the pending period counts.

Agreements That May Affect the Timeline

An installment agreement does not automatically extend the CSED by itself.

Still, appeals, defaults, or signed waivers tied to collection actions can affect timing, so every IRS form deserves careful review before signature.

How the 10-Year Statute Interacts With IRS Collection Tools

Before the CSED expires, the IRS can use an IRS levy to take funds or property to satisfy the debt. That power includes a bank levy, wage garnishment, and seizure of certain assets in more serious cases.

A federal tax lien works differently. The lien is the government’s legal claim against your property, while a levy is the actual taking of money or assets.

Those concepts overlap but are not identical.

A Notice of Federal Tax Lien can exist during the collection period, and collection pressure sometimes increases as the CSED gets closer because the IRS knows its window is closing.

Levies, Garnishments, and Liens in Plain English

A levy takes money, such as wages or bank funds, to pay tax. A lien is public notice that the government claims an interest in your property, which can complicate credit, refinancing, and sales.

Step-by-Step: What to Do If You Think You’re Near the 10-Year Mark

Start with transcripts, not assumptions.

Confirm each assessment date and each CSED because one tax year can contain multiple assessed amounts with different expiration dates.

Next, identify tolling events and document them.

Bankruptcy filings, CDP requests, and Offer in Compromise submissions can all change the calendar, and missing one event can throw off your estimate by months.

Then choose a resolution path that fits the facts.

If you need help with prior years taxes, compare options before filing forms that may affect timing, and review whether prior taxes support, hardship status, or a payment plan makes more sense.

Decision Guide for Common Scenarios

If collection is active and cash flow is stable, compare an installment agreement with other options based on cost and enforcement risk. If hardship is real, Currently Not Collectible status may stop active collection, but the IRS will want financial proof.

When to Get Professional Help

Complex files deserve expert review. Multiple years, prior bankruptcy, active levy notices, or a Final Notice of Intent to Levy can turn a simple 10-year question into a transcript analysis problem.

Real-World Examples: Calculating the Expiration Date

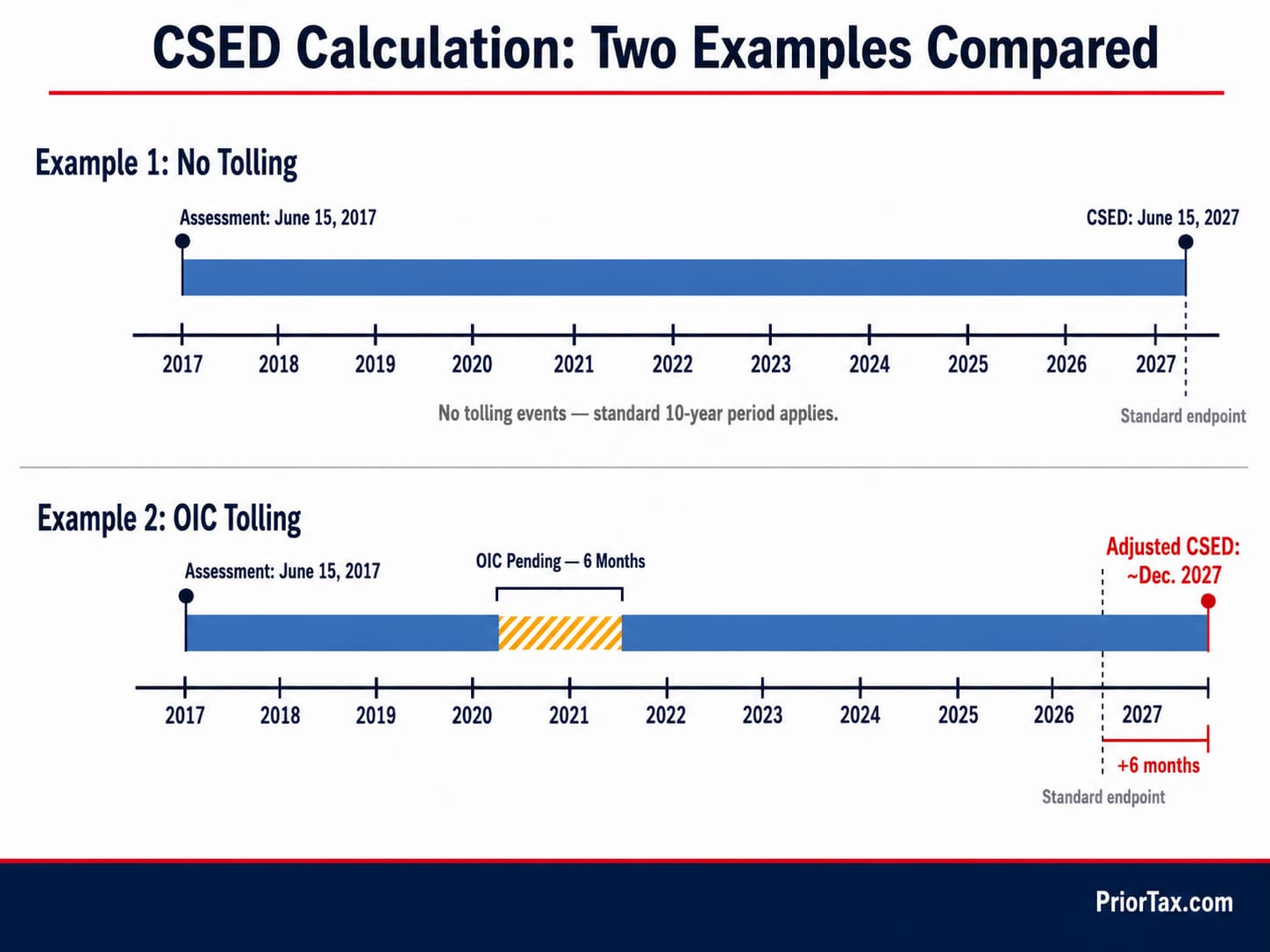

Example 1: A balance due return is processed and assessed on June 15, 2017. If no tolling occurs, the CSED is generally June 15, 2027, which shows why the return’s due date is not the legal starting point.

Example 2: The IRS assesses tax on June 15, 2017, and the taxpayer submits an Offer in Compromise in 2021 that remains pending for six months. That pending period can move the CSED roughly six months later, and the shift happens even if the offer is rejected.

Multiple assessments complicate one tax year. If an original return was assessed in 2017 and an audit added tax in 2019, each assessed amount may carry a different collection expiration date.

Example 1: Simple 10 Years From Assessment

Assessment date controls the clock. A 2017 assessment usually points to a 2027 CSED absent tolling, regardless of whether the tax year was much earlier.

Example 2: Tolling Extends the CSED

Pending time matters. A CDP hearing or Offer in Compromise can push the date out because the statute stops running while collection is suspended.

Common Mistakes and Risky Myths to Avoid

The “7-year rule” confuses tax debt with credit reporting concepts. IRS collection usually follows a 10-year period from assessment, and that period can run longer when tolling applies.

Not filing is another costly mistake.

Unfiled returns can lead to IRS-created balances through SFR procedures, and those assessments often overstate what you really owe because they omit taxpayer-favorable items.

Guessing the CSED is risky. If you act on the wrong date, you may ignore a live collection case or choose a strategy that does not match the actual timeline.

Practical Safety Checks Before You Act

Verify which years are assessed and which are still unfiled. If you missed a filing deadline, review tax deadline missed and filing taxes late because unfiled years can create fresh assessments later.

Track every IRS notice and appeal deadline.

The Right to Finality only helps if you preserve your rights on time, especially when levy or lien notices create short response windows.

Frequently Asked Questions (FAQs)

Can IRS come after you after 10 years?

Usually no, once the 10-year collection statute expires for a specific assessment. Tolling events such as bankruptcy, a CDP hearing, or an Offer in Compromise can extend that deadline.

How far back can the IRS go after you for not filing taxes?

If you do not file, the normal three-year assessment limit may not apply. The IRS can assess unfiled years later and may use a Substitute for Return.

Do you still owe the IRS after 7 years?

Yes, often you do. The seven-year idea is commonly confused with credit reporting, while IRS collection is generally tied to a 10-year period from assessment.

Can the IRS go back past 7 years?

Yes. Assessment and collection can reach beyond seven years depending on when tax was assessed, whether returns were unfiled, and whether the statute was paused.

The core rule is simple, but the real answer lives in the transcript. Once you know the assessment dates, tolling events, and CSED for each balance, the IRS timeline stops being a rumor and becomes a calendar you can actually use.

Categories: